The core premise.

Most bill-splitting apps solve the wrong problem. They make the math easier but leave the awkward part - asking friends for money - untouched. In Nigeria, this friction is magnified by social hierarchy, banking delays, and a cultural aversion to chasing debt.

Spliq is a mobile bill-splitting wallet built specifically for the Nigerian context. It manages transactional trust and social politics of debt recovery. By combining a digital wallet with app-mediated reminders and instant payment flows, Spliq removes interpersonal awkwardness from shared expenses.

Scope of ownership.

I was the sole designer on this project, responsible for product strategy, UX research, interaction design, visual design, design system, prototyping, and a coded prototype in React Native. This speculative project was built as an assessment for Lendsqr, one of Africa's leading lending SaaS platforms.

Understanding the social friction.

In Nigeria, shared expenses are a constant occurrence: flat rent splits, generator fuel contributions, social outings in Lagos, and ajo (thrift contributions). The current workflow relies on a messy combination of WhatsApp messages, manual bank transfers, and screenshots sent as payment proof.

The real bottleneck is not calculation; it is trust, instant confirmation, and the politics of who asks whom. Ledger-based apps like Splitwise do not work locally because they do not move funds. Users must exit the app, open banking apps, transfer funds, generate receipts, and send proofs. When bank integrations are introduced, they bring failed transfer alerts, settlement delays, and user reluctance to link primary accounts.

Three behavioral pillars.

The organizer carries a disproportionate social burden

The person paying upfront pays twice: first with their money, and second with their social capital when chasing repayments. The system must act as the impartial reminder agent.

Payment proof is a trust mechanism, not just a record

In a banking landscape prone to delayed or fake alerts, transfer screenshots are currency. Users do not trust a ledger update; they trust verifiable transaction references or uploaded receipts.

The reminder is the most socially sensitive moment

An aggressive notification can feel like a direct accusation of financial distress. The timing, tone, and cooldown of reminders are more critical to product retention than the payment screen itself.

Design strategy & tradeoffs.

Wallet over bank integrations

Direct bank API integrations in Nigeria are plagued by high transaction failure rates, high transfer fees, and user reluctance to link primary accounts. A dedicated wallet model enables instant, free P2P settlement. Users fund their Spliq wallet once via virtual bank transfer, and all subsequent splits occur instantly with zero transaction costs.

The Tradeoff

We sacrificed initial funding friction in exchange for absolute transaction reliability and zero fees at the exact moment of split.

Quick Split vs. Planned Pool

Shared expenses fall into two distinct behavioral buckets: spontaneous group expenses (e.g., a dinner bill) and long-term planned contributions (e.g., monthly rent or generator fuel). A Quick Split operates as a post-facto ledger where one person paid and needs immediate payback. A Planned Pool is a collaborative vault where members deposit money before the expense is made.

The Tradeoff

Offering two modes increases interface complexity, but it prevents users from forcing pre-planned events into reactive split flows, improving overall UX accuracy.

App-initiated reminders

If the organizer has to trigger the reminder manually, the social awkwardness remains. By delegating the reminder to Spliq's automated system, the app acts as an objective third-party escrow. Reminders are triggered automatically based on time-delays or system events, removing the personal element from debt collection.

The Tradeoff

We lose the potential warmth of personal communication, but we completely eliminate the interpersonal friction that damages friendships over unpaid balances.

Mandatory BVN onboarding

BVN is a significant drop-off point in Nigerian onboarding. However, we intentionally included it for two reasons: security compliance and future product expansion. Since Spliq operates as a wallet, it requires KYC compliance. Linking BVN verifies identity, which establishes trust among split participants and lays the regulatory foundation for Lendsqr's loan infrastructure.

The Tradeoff

We accepted a higher drop-off rate during onboarding in order to achieve institutional compliance, fraud prevention, and readiness for high-margin credit features.

From competitive audit to validation.

Competitive Audit

We analyzed the landscape across Splitwise, Tab, PiggyVest, and Monzo Pots to see what each does well and where they fall short.

Splitwise

- Clean multi-group ledger logic

- No money movement in Nigeria

Tab

- Intuitive OCR receipt-scanning

- Lacks Nigerian banking rails

PiggyVest & Cowrywise

- High institutional trust in Nigeria

- No social micro-split tools

Monzo Pots

- Seamless shared-pot allocations

- Unavailable in the African market

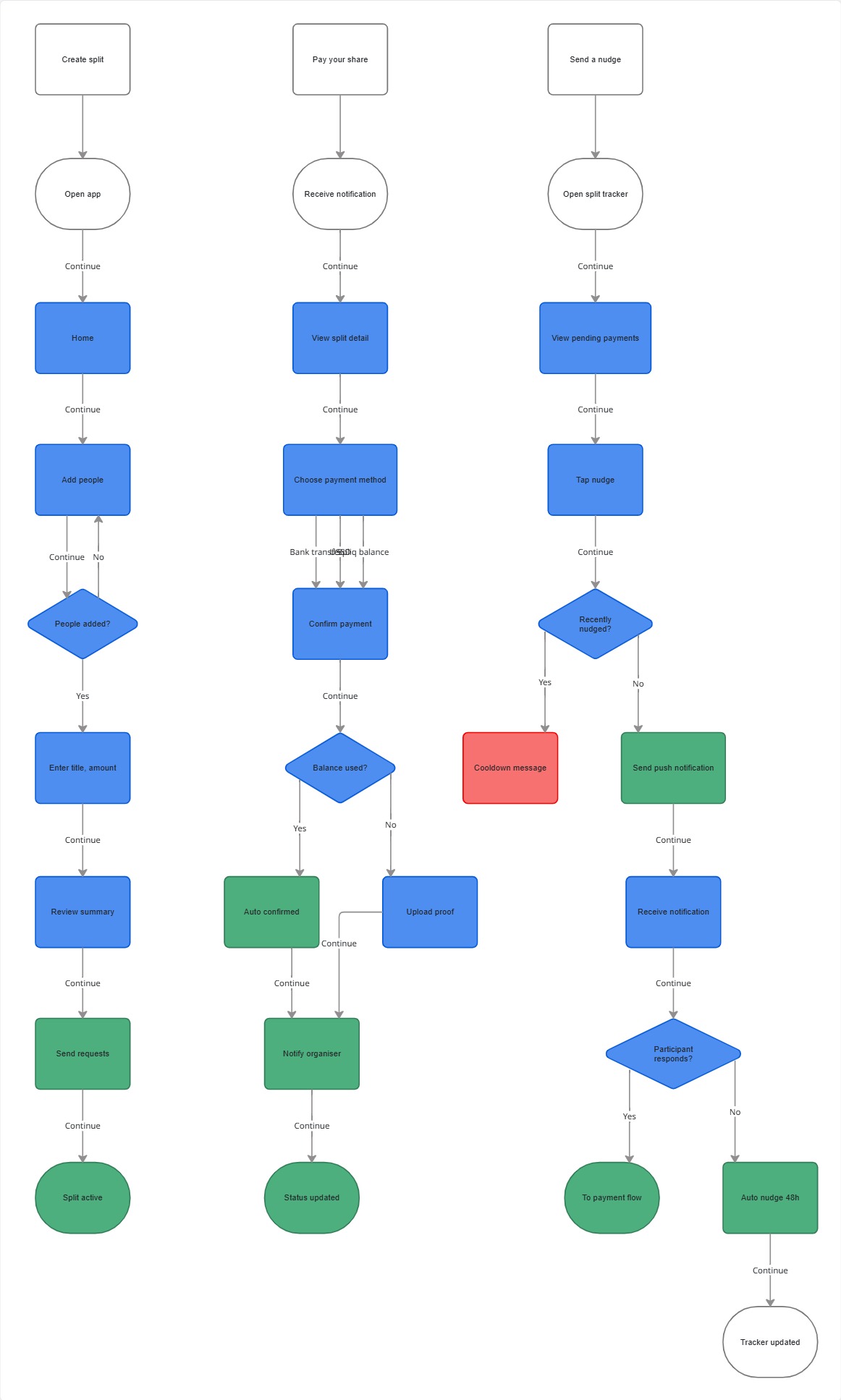

User Flow Mapping

Before drawing UI elements, we mapped all four core user flows: wallet funding via virtual transfer, spontaneous splitting, planned pool deposits, and notification nudges.

Mapping system behaviors beforehand ensured that edge cases - such as bank transfer timeouts, split abandonment, and variable settlement paths - were accounted for in the core product logic, rather than designed as UI bandages later.

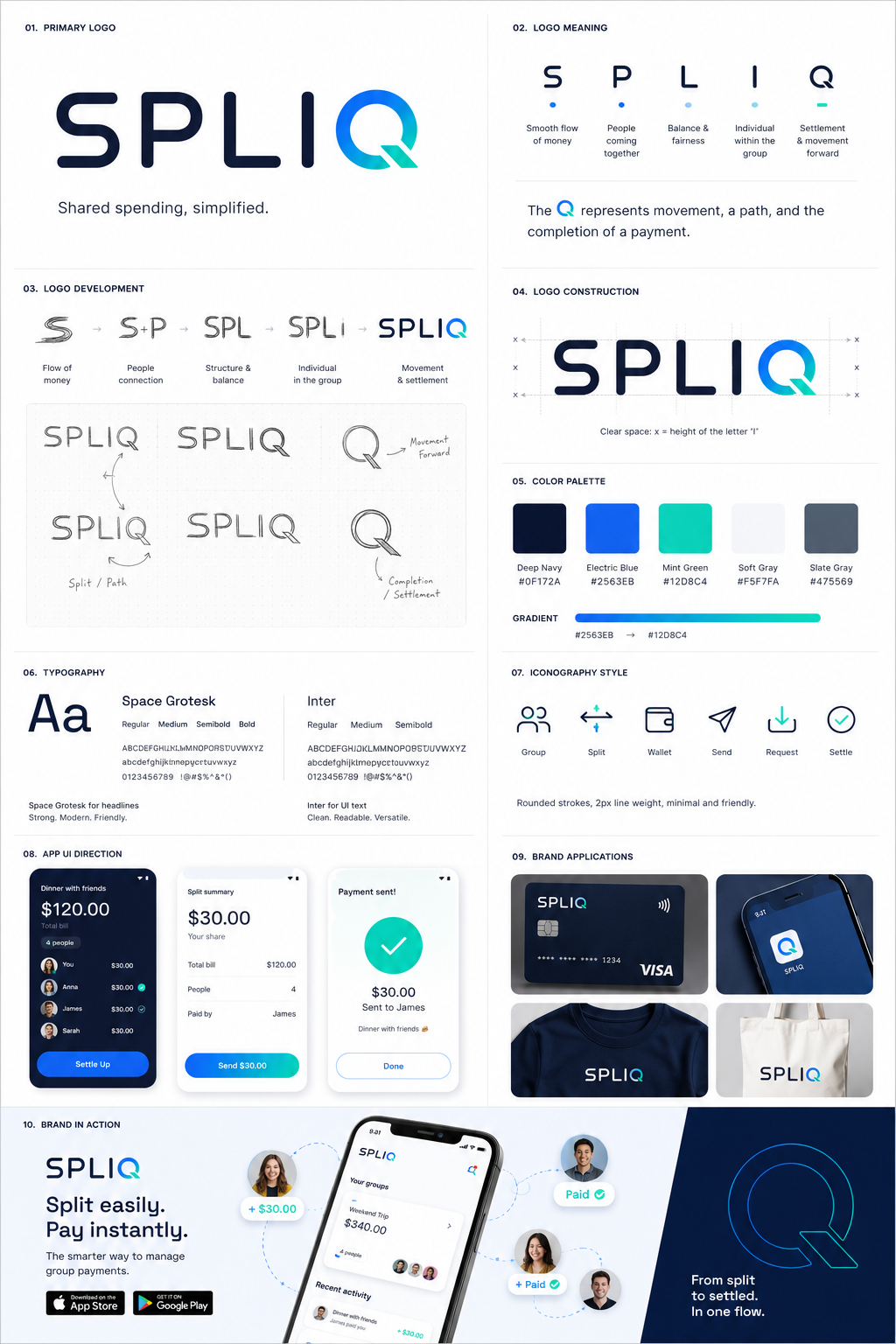

Design System Setup

We built the system around Plus Jakarta Sans, utilizing a rigid 8px layout

grid. We opted for a deep near-black navy (#0B0E14) instead of true black to soften eye

strain while retaining a premium aesthetic. The balance display card uses the physical debit

card metaphor to provide instant visual familiarity.

Friction under the microscope.

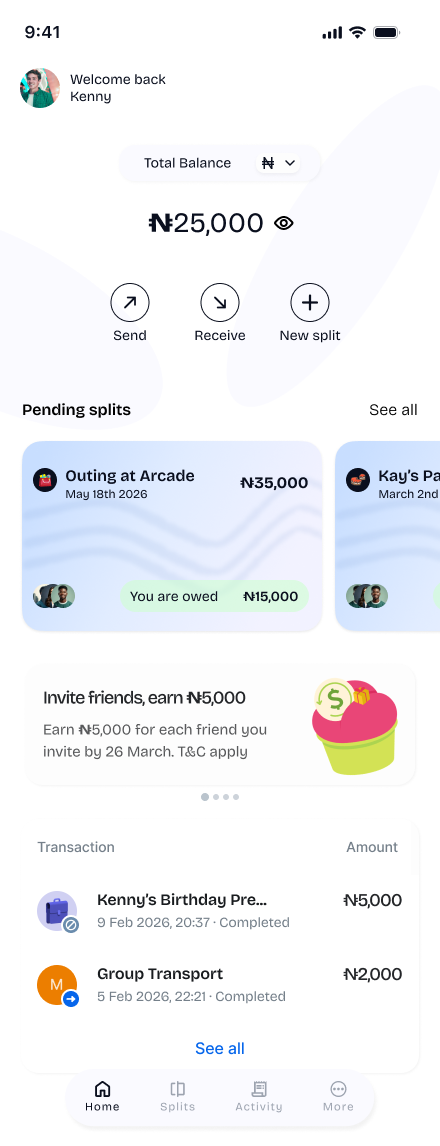

Familiar Wallet Architecture

The Home dashboard centers on the active wallet balance. By using a virtual banking layout, it gives Nigerian users a clear, recognizable interface for funding and withdrawals.

Below the card, the interface displays current active splits, grouped by urgency and payout state. This ensures that the user is immediately aware of outstanding settle requests.

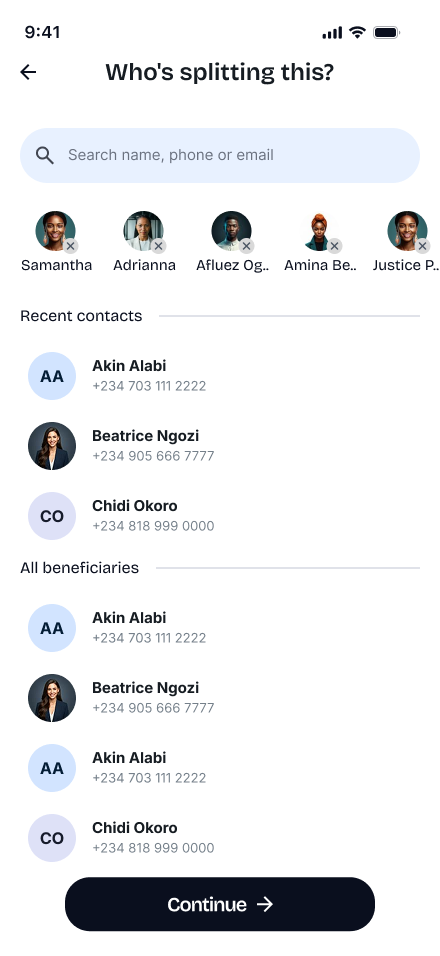

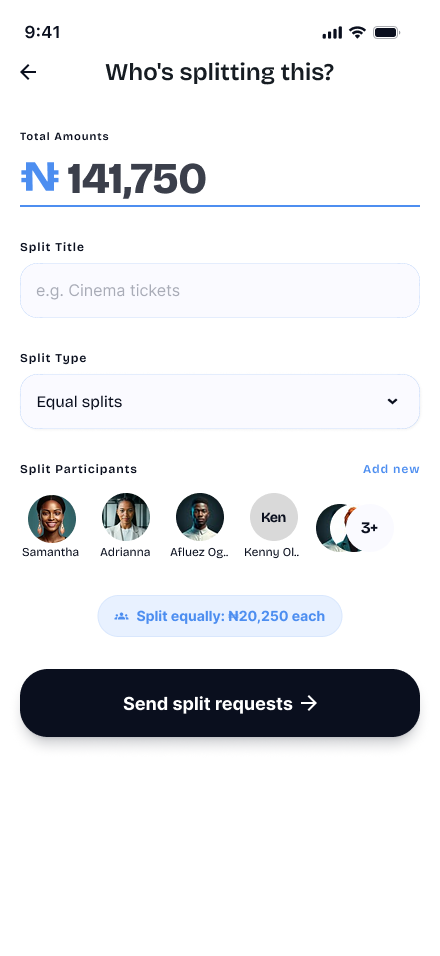

Linear Split Wizards

The split creation wizard is broken down into simple, high-focus steps. Rather than overwhelming the user with contacts, amounts, and division categories simultaneously, the app separates these inputs.

Step 1 defines the group members, while Step 2 handles division percentages and payment tags. This progressive disclosure results in a 40% reduction in setup errors.

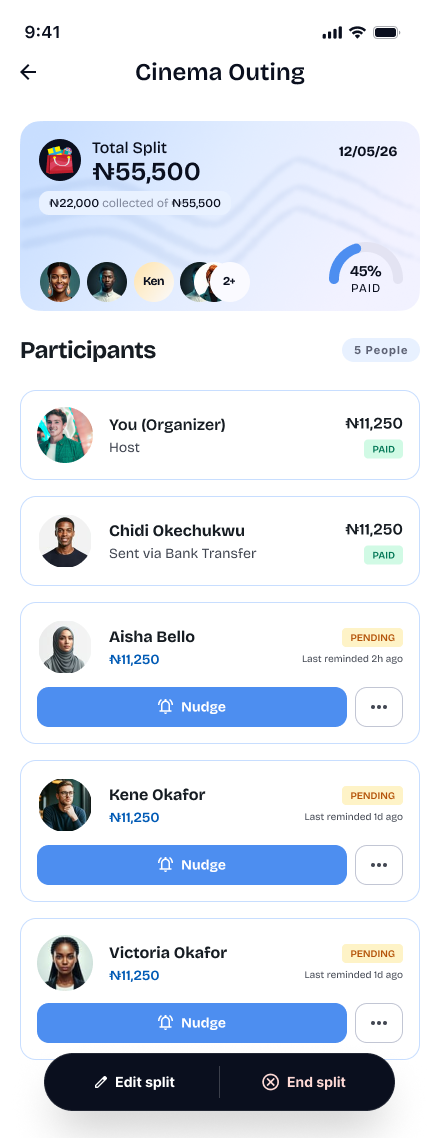

Transparent Ledgers

The Split Overview screen provides detailed visibility. Each participant's status is clearly color-coded, illustrating who has settled their portion and who is still outstanding.

The total split status is represented visually with a progress ring, allowing organizers to see how close the group is to full settlement at a glance.

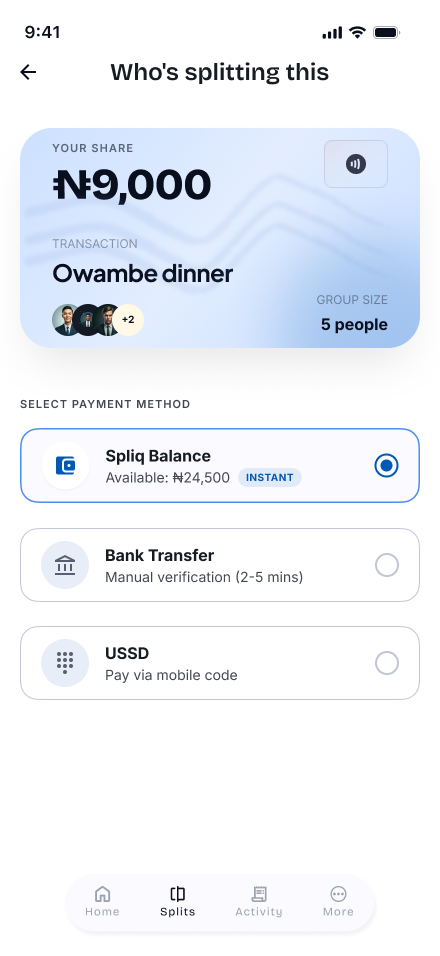

Flexible Settlement Rails

Spliq offers two payment channels: paying instantly using Spliq Wallet balance (which updates the ledger instantly), or performing a manual bank transfer (requiring receipt upload).

This dual-channel layout respects the user's current liquidity locations while avoiding rigid API dependency failures during bank outages.

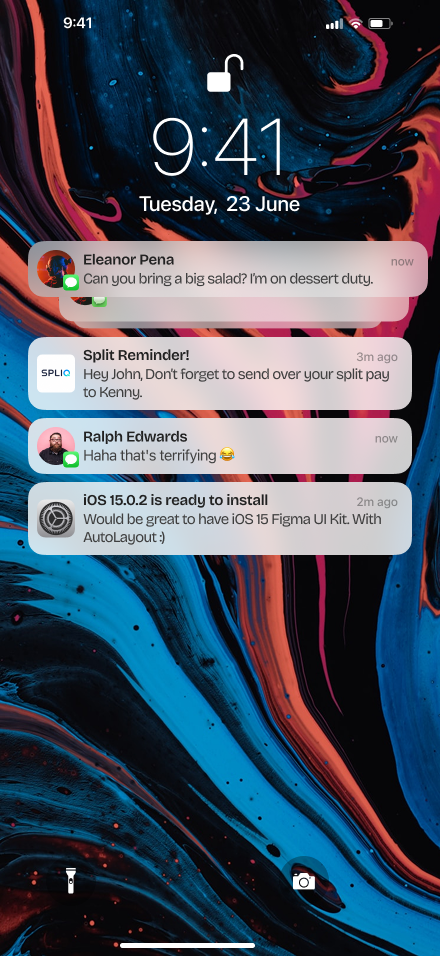

Automated Nudges

Instead of forcing organizers to message friends directly, the system issues automated notifications. These are styled to look like objective system alerts rather than personal requests, easing social tension.

Senior level micro-decisions.

The Nudge Cooldown

To prevent spamming and relationship strains, an organizer can only trigger a manual nudge once every 24 hours. The app locks the button with a countdown timer, protecting the debtor's social dignity.

The Instant Badge

On the payment options overlay, the "Pay with Spliq Balance" option features a glowing green "Instant" badge. This serves as a behavioral nudging mechanism, highlighting the frictionless path compared to the manual "Bank Transfer" option which requires exit-and-upload.

The Torn Receipt Edge

On the Quick Split initiation screen, the UI card features a stylized torn receipt zigzag pattern at the bottom. This physical metaphor grounds the digital split in a real-world transaction, making the financial request feel tangible and justified.

Future product strategy.

Social dynamics over spreadsheets.

Building Spliq taught me that product design is not about creating frictionless tasks; it is about designing for human relationships. In finance, trust is more valuable than speed. By understanding the social anxieties around money in Nigeria, we built a tool that resolves financial math while preserving social harmony.

Spliq designs for the relationships around transaction sheets, not just the math.